When you’re considering investing your money in mutual funds, something that comes to mind a lot is deciding between regular and direct plans. Both can increase your money, but there’s a significant difference that influences your return: the expense ratio. If you are new to all this, then the expense ratio is essentially the charge the fund incurs to invest your money, and it can have a significant effect on the long term.

In this blog post, we’ll differentiate between direct and regular mutual funds, with a particular focus on their expense ratios as of 2025 in India. We’ll keep it easy, just like talking with a friend, so that you can make choices that are right for your wallet.

What Are Regular Mutual Funds?

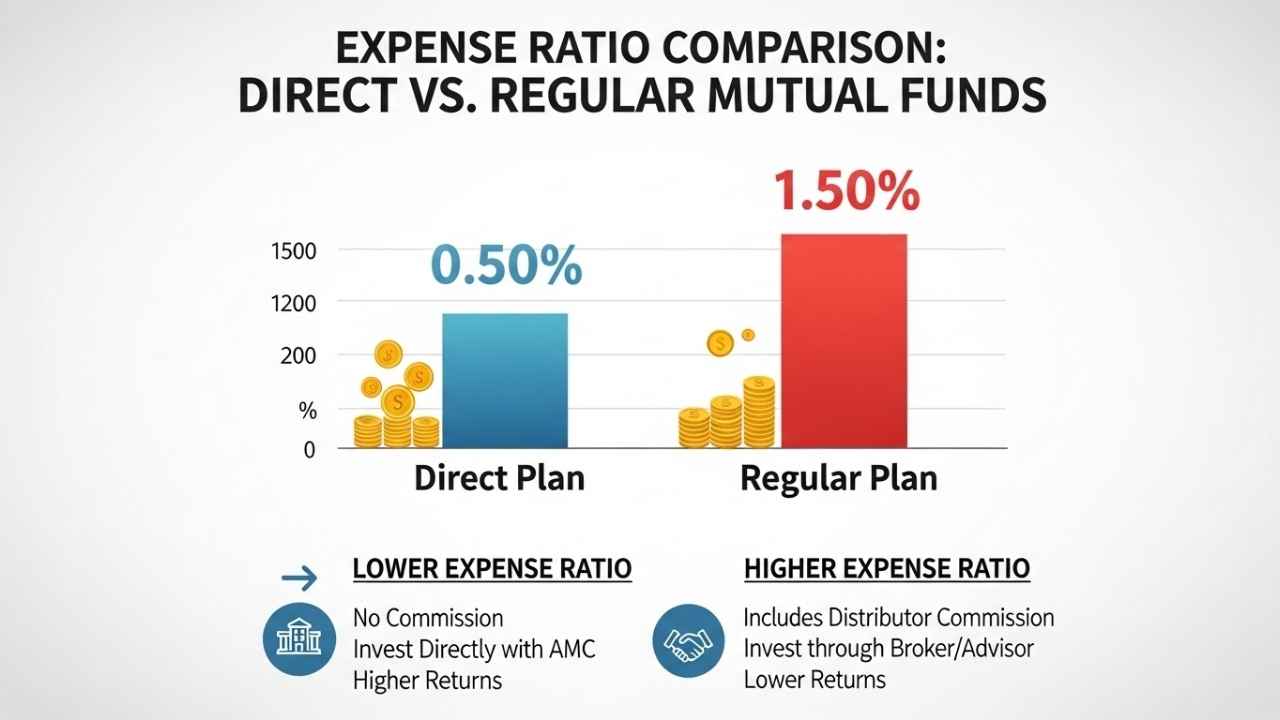

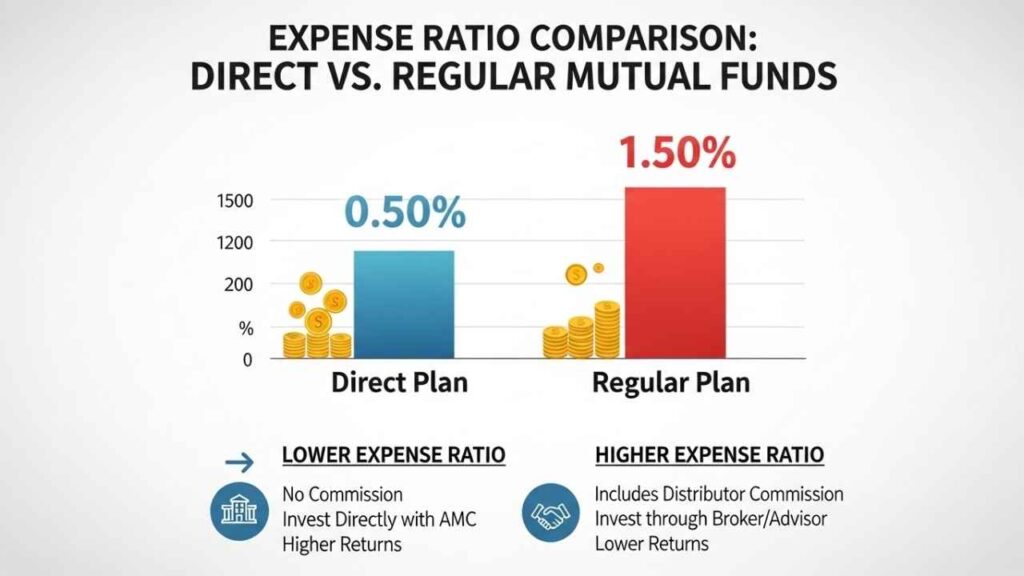

Regular mutual funds are the conventional method by which most individuals invest. You purchase them through a distributor, such as a bank, financial advisor, or online broker, which acts as a middleman. This middleman provides guidance, documentation, and continuous support, perfect if you’re new to it or don’t feel like doing everything yourself. Now, this is where the expense ratio comes in – this is the annual charge taken from the assets of the fund in order to pay for management fees, advertising, and yes, that commission paid to that distributor.

In 2025, the cost ratio for normal mutual funds is usually between 1.5% and 2.5% for equity schemes, and less for debt schemes, let’s say between 0.5% and 1.5%. Why so steep? A portion of that – usually 0.5% to 1% – is paid to the distributor’s commission. All this adds up over a period of time. For instance, if you invest ₹1 lakh in a fund with an expense ratio of 2% and it increases by 10% every year, after 10 years, you would have paid about ₹20,000 in fees alone. That’s money that was compounding for you! Regular plans are convenient for those who want professional advice, but if you are smart enough to do it yourself, you might wonder if there’s anything less expensive. And there is – but more on that later. In general, systematic funds are appropriate for do-it-yourself investors who value convenience over extracting every last rupee from returns.

What Are Direct Mutual Funds?

Direct mutual funds eliminate the middleman completely. You purchase them directly from the website, app, or office of the fund house, without any distributor or advisor in the middle. This implies zero commissions are paid to anyone, keeping things low-cost. SEBI launched direct plans way back in 2013, and now they are extremely popular in 2025, particularly among app users such as Groww or Zerodha, who invest their money.

The major gain is in the expense ratio being lower. As there’s no distributor charge, direct plans cut down by approximately 0.5% to 1% from regular ones. For equity schemes, you may find ratios between 0.5% to 1.5%, while debt schemes can be as low as 0.2% to 1%. Use the same ₹1 lakh investment growing at 10% – with a 1% expense ratio, your charges over 10 years come down to about ₹10,000, leaving more for growth. That saving can grow into lakhs over generations! Direct plans are the way to go if you’re willing to do your own research on funds, read the fact sheets, and monitor the performance. No hand-holding, but platforms have tools such as calculators and comparison facilities now to make it simple. In brief, for maximum return and lowest costs, go for direct – provided you are willing to exert a little extra effort along the way.

Comparison Table: Expense Ratios at a Glance

To make it clearer, here’s a simple table comparing the typical expense ratios for direct and regular mutual funds across common categories in India as of 2025. These are averages based on current data – always check the latest from the fund house for exact figures.

| Fund Category | Regular Plan Expense Ratio (Range) | Direct Plan Expense Ratio (Range) | Average Difference |

|---|---|---|---|

| Equity Funds | 1.5% – 2.5% | 0.5% – 1.5% | 1.0% |

| Debt Funds | 0.5% – 1.5% | 0.2% – 1.0% | 0.5% – 0.8% |

| Hybrid Funds | 1.2% – 2.0% | 0.4% – 1.2% | 0.8% |

| Index Funds | 0.8% – 1.2% | 0.2% – 0.5% | 0.6% – 0.7% |

This table shows how direct plans consistently offer lower costs, which can lead to better long-term returns.

Learn More:

- Difference in Expense Ratio Between Direct and Regular Mutual Funds

- Best Small-Cap Index Funds

- 10 Debt Mutual Funds That Outperformed in the Last 1 Year with 10% to 24% Returns

- Best Mutual Funds for Senior Citizens

- Best Green Hydrogen Stocks in India

Conclusion

Ultimately, the primary distinction between direct and normal mutual funds comes down to the expense ratio – direct plans are less expensive as they avoid the distributor commissions, which can raise your returns by 0.5% to 1% per year. That may not sound like a lot, but years later, it adds up big time due to compounding. If you’re a do-it-yourselfer and like handling your investments, go direct to save on fees. But if you need guidance and hand-holding, regular plans may be worth paying extra for. Either way, begin investing early and be consistent. Remember that mutual funds carry market risks, so research or seek the services of an advisor. Good luck with your investing!

FAQ: Expense Ratios

What is the expense ratio in mutual funds?

The expense ratio is the yearly fee charged by the fund company to cover costs like management, administration, and marketing. It’s a percentage of your investment and gets deducted automatically, affecting your net returns.

Why is the expense ratio higher in regular mutual funds?

Regular funds include commissions for distributors who sell and advise on the funds. This extra cost pushes the ratio up by about 0.5% to 1% compared to direct plans.

Can I switch from regular to direct mutual funds?

Yes, you can switch via a process called “switch transaction.” It might trigger exit loads or taxes, so check with your fund house. It’s often worth it for long-term savings.

Are direct mutual funds better for everyone?

Not necessarily. They’re great for experienced investors who don’t need advice. Beginners might benefit from the guidance in regular plans, even with higher fees.

How do I check the expense ratio of a mutual fund?

Look at the fund’s fact sheet or scheme information document on the fund house website or platforms like AMFI India. It’s updated regularly, so always verify the latest figures.